TL;DR:

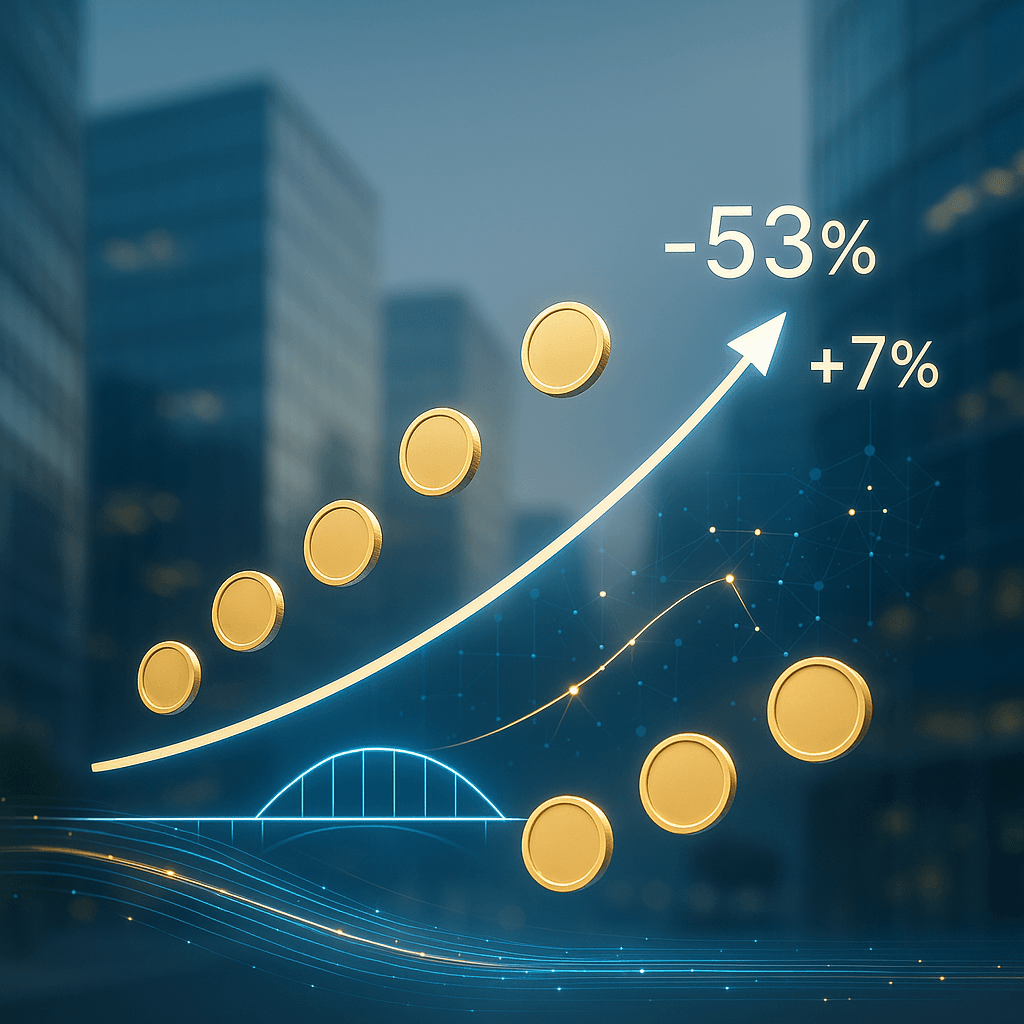

• Circle shares spike 7% after 53% revenue surge in first public earnings

• USDC stablecoin circulation exploded 90% to $61.3B, capturing market share from Tether

• New Arc blockchain launch targets enterprise payments and capital markets

• Results validate stablecoin adoption thesis amid crypto market maturation

Circle Internet Group just delivered a markets-moving debut as a public company, with shares surging 7% in premarket trading after the stablecoin giant reported a stunning 53% revenue jump to $658.1 million. The blowout Q2 results, driven by explosive 90% growth in USDC circulation, signal that institutional adoption of digital dollars is accelerating faster than even bulls predicted.

Circle Internet Group just proved that the stablecoin revolution isn't coming – it's here. The company's first earnings report as a publicly traded entity sent shares rocketing 7% in premarket trading, with revenue surging 53% year-over-year to $658.1 million in Q2 2025. The numbers validate what insiders have been whispering: institutional money is flooding into dollar-backed cryptocurrencies at an unprecedented pace.

The real story lies in USDC's explosive growth trajectory. Circle's flagship stablecoin saw circulation skyrocket 90% to $61.3 billion, directly challenging Tether's stranglehold on the market. According to CryptoQuant data, USDC now commands 26% of the dollar-backed stablecoin market, up from roughly 14% just two years ago, while Tether's dominance has slipped to 67%.

"We're seeing unprecedented demand from institutions who want regulatory clarity and transparency," CEO Jeremy Allaire told analysts during the earnings call. The comment underscores how Circle's New York Stock Exchange listing in June has positioned it as the "clean" alternative to Tether, which continues facing regulatory scrutiny.

But the earnings also revealed the true cost of going public. Circle swung to a net loss of $482.1 million, or $4.48 per share, compared to earnings of $32.9 million a year ago. The red ink came primarily from $424 million in stock-based compensation and $167 million in convertible debt adjustments – classic IPO growing pains that investors are brushing aside in favor of the revenue momentum.