A stunning revelation buried in Nvidia's latest SEC filing exposes the chipmaker's heavy dependence on just two mystery customers who collectively drove 39% of its record $46.7 billion Q2 revenue. The disclosure raises critical questions about revenue concentration risk as the AI boom reaches unprecedented heights.

Nvidia's latest SEC filing just dropped a bombshell that Wall Street is still digesting. Behind the chipmaker's record-breaking $46.7 billion Q2 revenue lies an uncomfortable truth: nearly 40% of that massive haul came from just two customers, cryptically labeled "Customer A" and "Customer B" in regulatory documents.

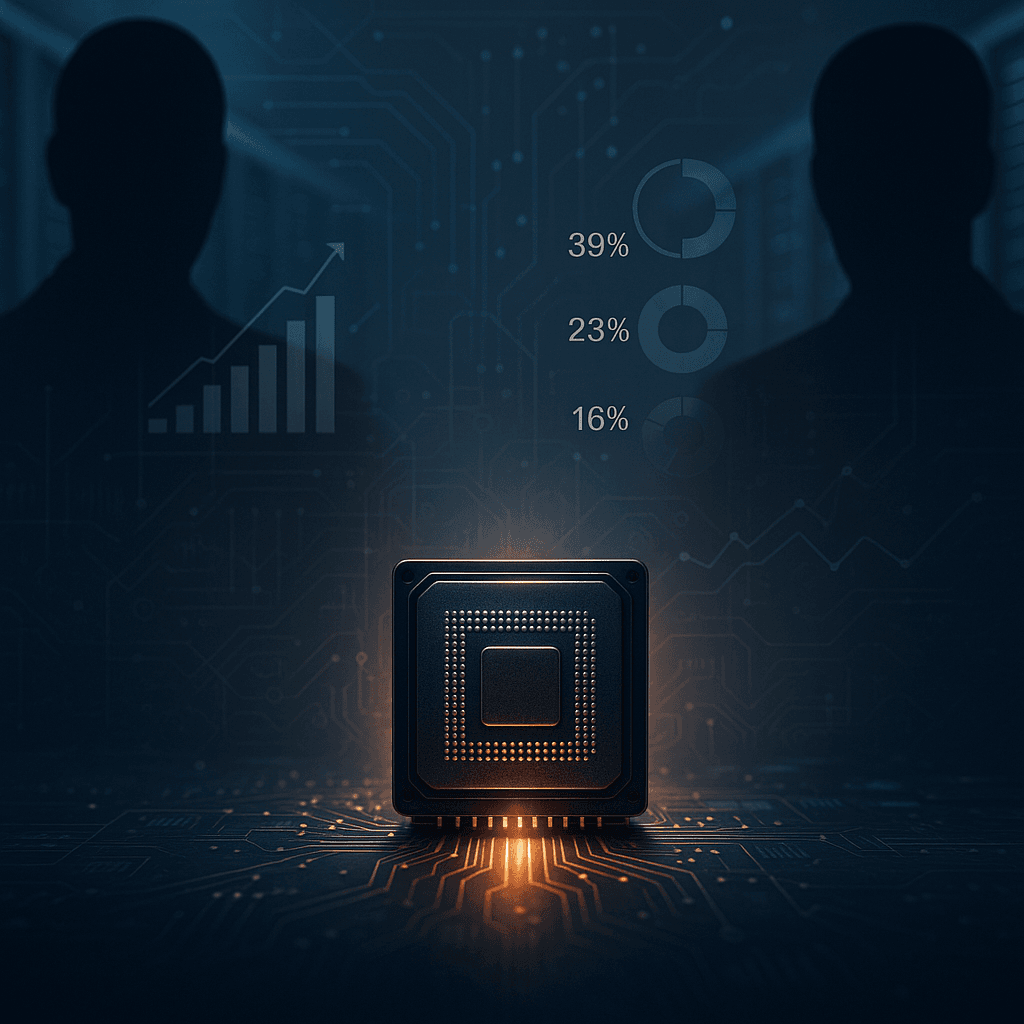

The numbers are staggering. Customer A alone accounted for 23% of total Q2 revenue – roughly $10.7 billion – while Customer B contributed another 16%, or about $7.5 billion. Combined, these two entities generated more revenue for Nvidia than many Fortune 500 companies see in an entire year.

But here's where it gets interesting. These aren't the household names you'd expect. Nvidia clarifies in its filing that these are "direct" customers – original equipment manufacturers, system integrators, or distributors who purchase chips directly from the company. The tech giants everyone assumes are driving AI demand – Microsoft, Google, Amazon, Meta – are actually "indirect" customers buying through these intermediaries.

"Large cloud service providers accounted for 50% of Nvidia's data center revenue," CFO Nicole Kress revealed during earnings calls, according to CNBC reporting. Since data centers represented 88% of total company revenue, the math reveals just how concentrated this AI gold rush has become.

The customer concentration extends beyond the top two. Four additional customers accounted for 14%, 11%, another 11%, and 10% of Q2 revenue respectively. That means just six customers now drive 85% of Nvidia's quarterly revenue – a level of concentration that would make any CFO nervous.

For context, during the first half of fiscal 2026, Customer A and Customer B maintained their dominant positions at 20% and 15% of total revenue respectively. This consistency suggests these aren't one-time bulk purchases but sustained, strategic relationships that have become central to business model.