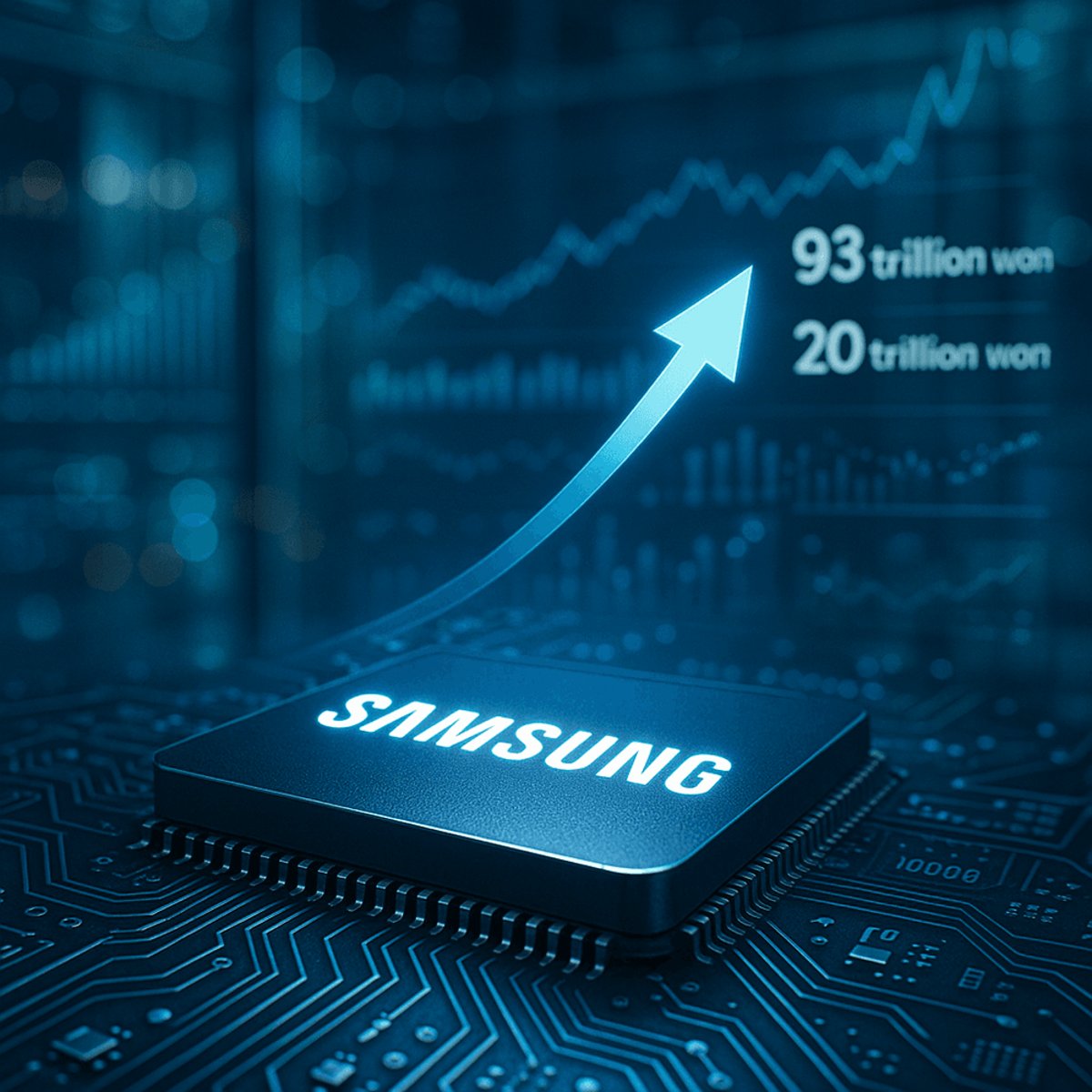

Samsung Electronics just lifted the curtain on what looks like a serious recovery story. The electronics giant's Q4 2025 earnings guidance points to consolidated sales of approximately 93 trillion Korean won and operating profit of around 20 trillion won - numbers that suggest the chip market's turning a corner after a rough stretch. That's a meaningful jump from both the previous quarter and last year's fourth quarter, signaling that demand for semiconductors and consumer electronics is heating up.

Samsung Electronics just put a stake in the ground about where the chip market's heading. The company's Q4 2025 earnings guidance shows consolidated sales hitting approximately 93 trillion Korean won and operating profit landing around 20 trillion won, based on K-IFRS accounting standards. That's the kind of guidance that makes investors sit up and take notice.

The real story lives in the comparisons. Samsung's Q4 operating profit guidance of 20 trillion won absolutely dwarfs last year's Q4 result of just 6.49 trillion won - that's more than a tripling of profitability. Sales are up 22.6% year-over-year, jumping from 75.79 trillion won in Q4 2024 to the 93 trillion won guidance for Q4 2025. For an industry that spent much of 2024 dealing with oversupply and weak demand, these numbers suggest something's fundamentally shifted.

The momentum's been building. Samsung's Q3 2025 already showed the company pulling in 86.06 trillion won in sales with 12.17 trillion won in operating profit, signaling the recovery wasn't just a one-quarter fluke. The progression from Q3 to Q4 guidance suggests the company's accelerating as the quarter winds down, which typically means stronger demand from smartphone makers, data center operators, and consumer electronics manufacturers.

The semiconductor business has been the focus here. After the brutal 2023-2024 period when memory chip prices collapsed and demand stayed weak, DRAM and NAND flash markets are finally tightening up. Samsung's a heavyweight in memory chips - it's one of the only companies that can compete at scale with SK Hynix and Micron. When Samsung's numbers start looking this strong, it's usually because the entire sector's benefiting from a structural shift in supply-demand dynamics.

The Q4 guidance also captures the strong consumer demand heading into the holiday season and early 2025. We've seen flagship phone launches, PC refreshes driven by AI features, and data center buildouts continue at a clip. Samsung makes the DRAM that powers servers, the NAND that stores data, and the chips inside everything from Galaxy phones to TVs. That diversification means when multiple markets heat up simultaneously, the numbers get really interesting.

Worth noting: Samsung's being precise with the guidance numbers because Korean disclosure regulations require it. The company's reporting these as medians from estimate ranges - sales between 92 trillion and 94 trillion won, operating profit between 19.9 trillion and 20.1 trillion won. That's a pretty tight band, suggesting Samsung's visibility into orders is solid heading into the new year.

The timing matters too. This guidance drops right as the industry's gearing up for 2026 product cycles and investment plans. For Apple, Google, and Samsung itself (through its device business), these memory and processor numbers directly impact what they can produce and sell. The guidance essentially signals that Samsung doesn't expect a cliff in demand - the opposite, actually.

This earnings guidance becomes the benchmark other memory chip makers will be measured against. When the sector's biggest players show 208% year-over-year operating profit growth, it ripples through supply chains and investor portfolios. We're likely to see similar strength from SK Hynix and potentially Micron when they report, but Samsung's leading the conversation right now about where the market's really heading in 2026.

Samsung's Q4 guidance is telling us that the semiconductor recovery we've been hearing about since mid-2024 isn't a false dawn. Operating profits more than tripling from a year ago, combined with solid quarter-over-quarter growth momentum, paints a picture of a company whose core chip businesses are firing on all cylinders. For the broader semiconductor industry, that's validation that the worst of the downcycle is behind us. For investors watching memory chip makers and the companies that depend on them, this is the kind of signal that shapes capital allocation decisions for the next cycle.