Microsoft just closed its worst quarter on Wall Street since the 2008 financial crisis, losing nearly a quarter of its market value as investors pump the brakes on AI infrastructure spending. The sell-off has reset the tech giant's earnings multiple to levels not seen since late 2022, before the generative AI boom began. The dramatic reversal marks a turning point in how Wall Street values AI investments, with one analyst noting that 'Redmond is in a pickle' as questions mount about when massive AI capital expenditures will translate into meaningful returns.

Microsoft is bleeding value at a rate not seen since the depths of the financial crisis. The company's stock has cratered nearly 25% this quarter, wiping out hundreds of billions in market capitalization and forcing Wall Street to fundamentally reassess how it values AI investments.

The carnage represents more than just a market correction. It's a referendum on Microsoft's massive bet on artificial intelligence infrastructure. The company has poured tens of billions into data centers, GPUs, and AI capabilities, but investors are increasingly skeptical about when - or if - those investments will generate proportional returns. According to CNBC's reporting, the sell-off has compressed Microsoft's earnings multiple to the lowest level since late 2022.

That timing is significant. Late 2022 was before OpenAI launched ChatGPT, before the AI arms race kicked into overdrive, and before Microsoft committed to what CEO Satya Nadella called the company's most important platform shift since the cloud. The valuation reset essentially erases the AI premium that Wall Street had built into the stock.

'Redmond is in a pickle,' one analyst noted in the CNBC coverage. The company faces a classic catch-22: slow AI spending and risk losing competitive ground to Google and Amazon, or maintain the investment pace and watch margins compress further.

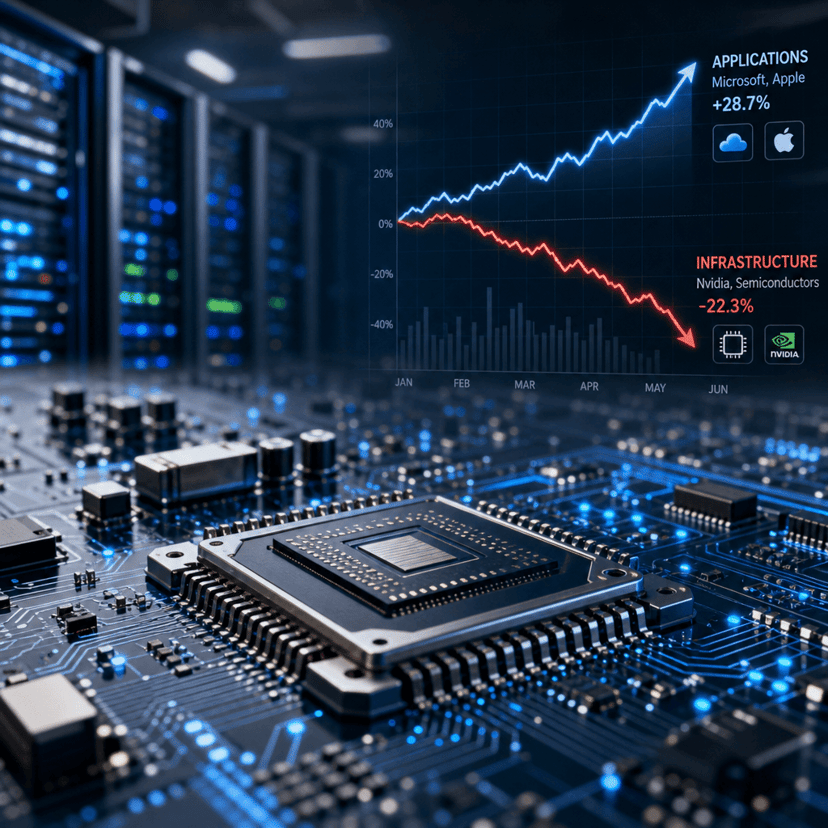

The pressure is mounting across multiple fronts. Microsoft's Azure cloud division, once the crown jewel delivering consistent 40%+ growth, has seen expansion rates moderate as AI infrastructure costs balloon. The company's $13 billion investment in OpenAI looked visionary 18 months ago, but now investors are questioning whether Copilot subscriptions and API usage will ever justify the expenditure.

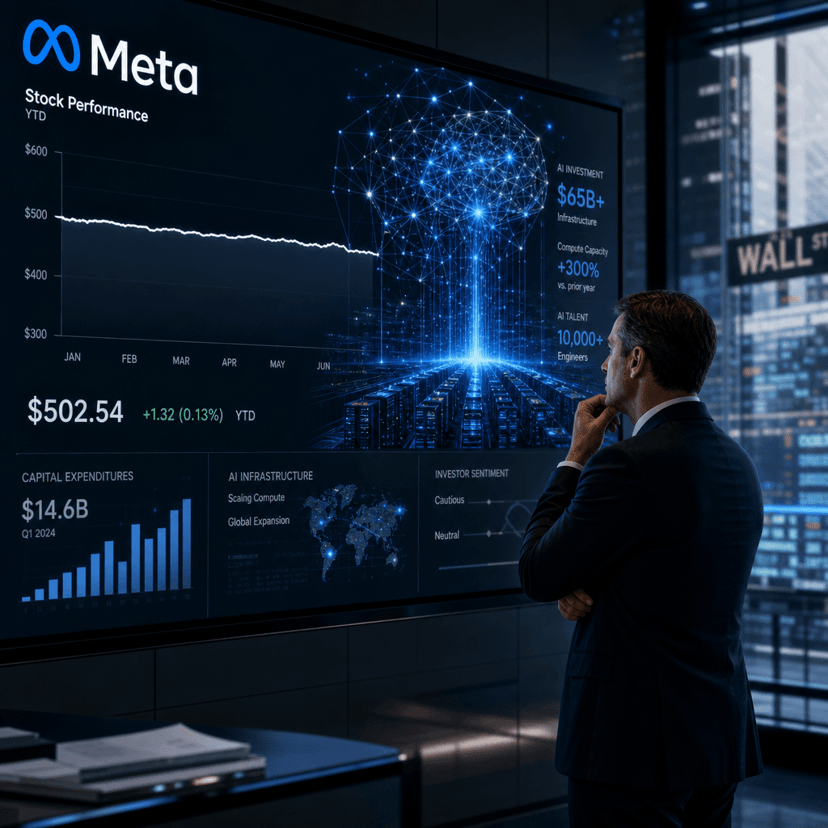

Competitive dynamics aren't helping. While Microsoft stumbles, Amazon Web Services has been gaining cloud market share, and Google Cloud is showing stronger profitability improvements. Meta has meanwhile demonstrated that you can build cutting-edge AI capabilities while maintaining disciplined capital allocation, making Microsoft's spending spree look increasingly reckless.

The quarterly performance echoes the dark days of 2008, when Microsoft's stock tumbled alongside the broader market during the financial crisis. But this time the company isn't caught in a systemic meltdown - it's facing questions specific to its strategic choices. The AI infrastructure buildout that Nadella championed as transformational is now being scrutinized as potentially value-destructive.

Investors are demanding answers on several fronts: How quickly can Copilot adoption scale? What's the actual margin profile of AI workloads versus traditional cloud services? When will GPU utilization rates justify the massive capital commitments? The fact that Microsoft hasn't provided satisfactory responses is evident in the stock chart.

The valuation compression also reflects a broader market recalibration around AI economics. Early enthusiasm assumed that AI capabilities would command premium pricing and drive rapid enterprise adoption. Reality has proven messier, with companies carefully evaluating AI ROI before committing to expensive deployments. That cautious approach benefits nobody more than it hurts Microsoft, which bet big on fast, widespread AI integration.

Wall Street's message is becoming clear: prove it or pause it. The days of getting rewarded for AI ambition alone are over. Investors want to see concrete monetization, sustainable margins, and a credible path to returns that justify the investment scale. Until Microsoft can deliver those proof points, the stock is likely to remain under pressure.

The timing couldn't be worse for Nadella, who has spent years positioning Microsoft as the AI leader. The company's early partnership with OpenAI and aggressive Azure AI rollout were supposed to establish unassailable competitive advantages. Instead, Microsoft finds itself defending a valuation that's been cut by a quarter while competitors chip away at its cloud dominance.

Microsoft's historic quarterly collapse signals more than just a rough patch for one company - it represents a fundamental shift in how markets value AI investments. The 25% decline and valuation reset to pre-ChatGPT levels suggest investors are done rewarding potential and now demand proof of profitability. As Microsoft heads into earnings season, Nadella faces the difficult task of justifying continued AI infrastructure spending while Wall Street demands evidence that the spending will actually pay off. The answer Microsoft provides could set the tone for how all of Big Tech approaches AI investment going forward. For now, Redmond isn't just in a pickle - it's in a pressure cooker.