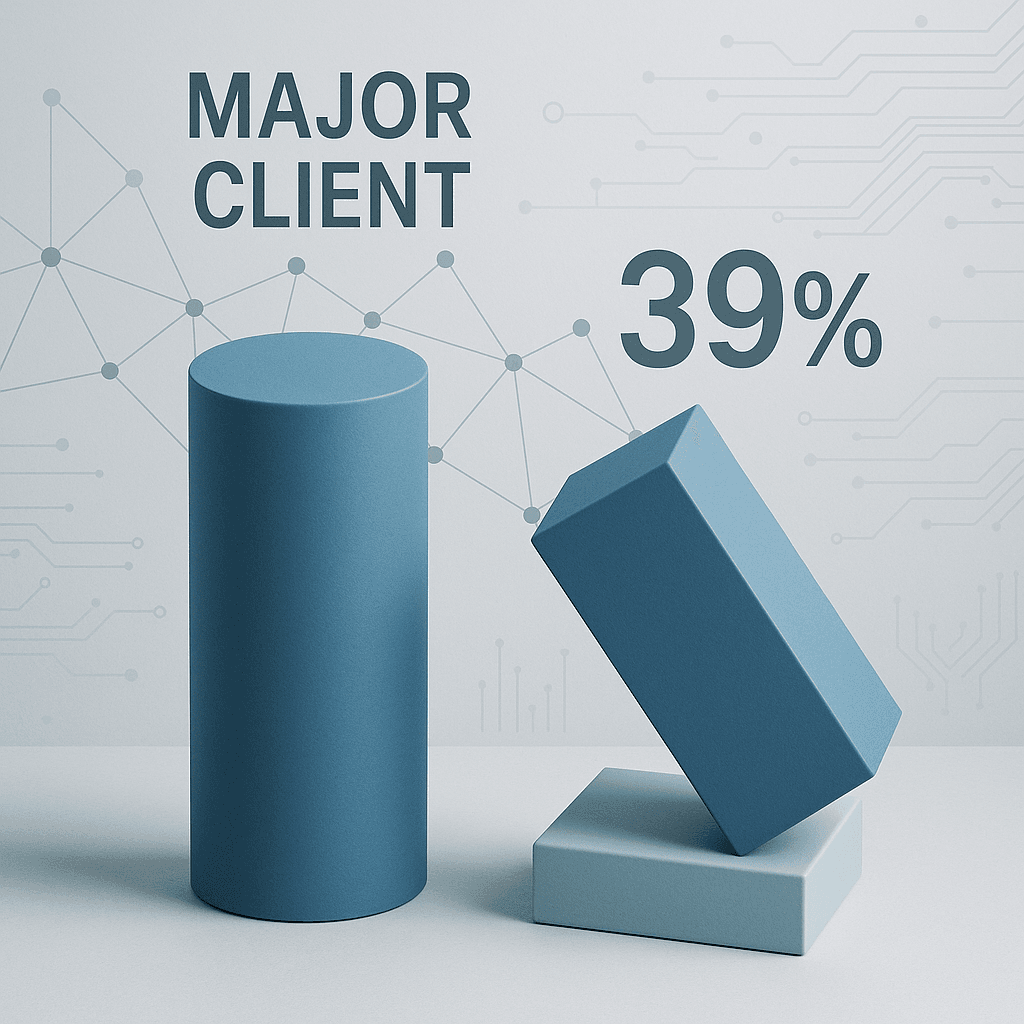

Nvidia just exposed a critical vulnerability hiding in plain sight. The AI chipmaker's latest SEC filing reveals two mystery customers now drive 39% of total revenue—up from just 25% a year ago. This dramatic concentration spike is reigniting Wall Street fears about the company's dependence on a handful of mega-buyers in an increasingly volatile AI market.

Nvidia just handed investors a double-edged sword wrapped in a quarterly filing. The AI chipmaker's latest SEC disclosure reveals that two anonymous customers—dubbed "Customer A" and "Customer B"—now account for a staggering 39% of total revenue, with Customer A alone representing 23% and Customer B contributing 16%. The numbers tell a story of both explosive growth and mounting risk. Just one year ago, Nvidia's top two customers represented a more manageable 14% and 11% of sales respectively according to previous SEC filings. That's a 56% increase in customer concentration during the company's most profitable year ever. The revelation sent a ripple of concern through Wall Street, where analysts are already questioning whether the AI boom can sustain its breakneck pace. "We see limited room for further earnings upside revision or share price catalyst in the near-term unless we have increasing clarity over upside in 2026 cloud service provider capex expectations," HSBC analyst Frank Lee wrote in a Thursday note, maintaining his hold rating on the stock. The mystery deepens when you dig into Nvidia's customer classification system. Customer A and Customer B are listed as "direct customers"—meaning they're not necessarily the end users burning through AI compute cycles. Instead, they're likely original equipment manufacturers like Foxconn or Quanta, or systems integrators like Dell that buy chips to build complete systems before selling to cloud providers and enterprises. This creates a complex web where the real AI demand could be coming from Microsoft, Amazon, Google, or Oracle, but flowing through these mysterious intermediaries. Adding another layer of intrigue, Nvidia revealed that two separate "indirect customers" each account for over 10% of total revenue, primarily buying systems through the same Customer A and Customer B channels. The company also disclosed that an "AI research and development company" contributed a "meaningful" amount of revenue through both direct and indirect channels—a description that has analysts speculating about everything from to emerging AI labs. Finance chief Colette Kress provided some context during Wednesday's earnings call, noting that "large cloud service providers" represent about 50% of data center revenue. Since data centers drive 88% of overall revenue, that means hyperscalers are still the dominant force behind the AI chip surge. But the concentration risk extends beyond just customer dependency. CEO Jensen Huang painted an ambitious picture of AI infrastructure scaling to $3-4 trillion by decade's end, with potentially capturing 70% of a typical $50 billion AI-focused data center's total cost. "As you know, the capex of just the top four hyperscalers has doubled in two years as the AI revolution went into full steam," Huang told investors, referencing an estimated $600 billion in combined spending commitments this year. The company is betting on diversification through "neoclouds"—specialized AI service providers challenging traditional hyperscalers—plus enterprise customers and sovereign AI initiatives that could generate $20 billion in revenue this year. Yet the latest filing suggests that despite this expansion rhetoric, revenue base is actually becoming more concentrated, not less. "We have experienced periods where we receive a significant amount of our revenue from a limited number of customers, and this trend may continue," the company acknowledged in its SEC filing—a remarkably candid admission for a company trading at premium valuations based on AI ubiquity assumptions. The timing couldn't be more critical as Wall Street increasingly models future based on cloud provider capital expenditure commitments rather than broader AI adoption metrics.