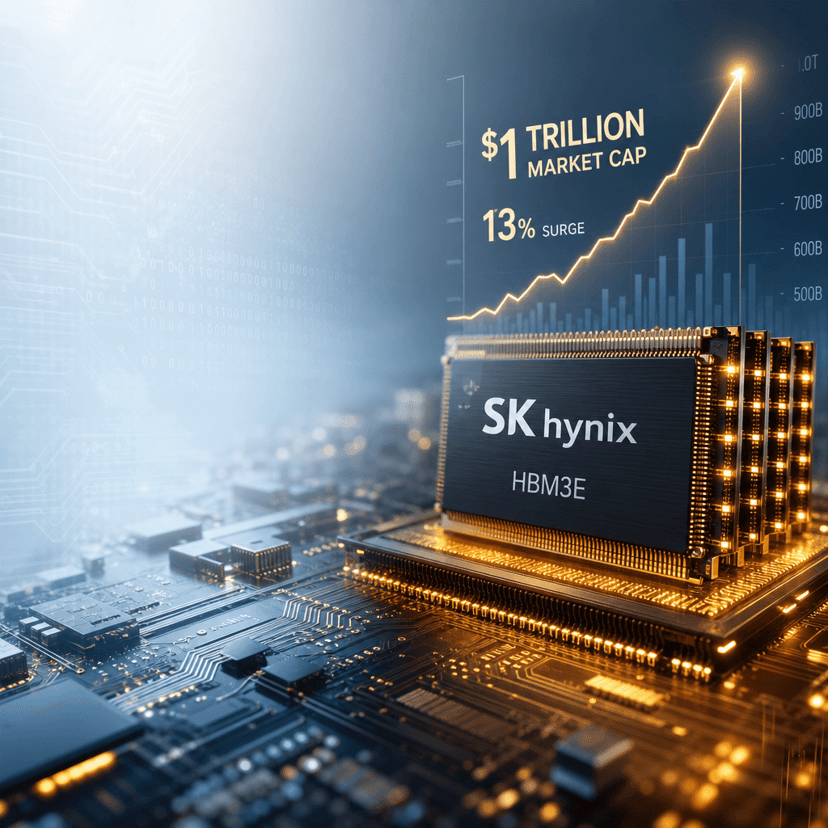

SK Hynix is having the kind of year that makes investors do a double-take. The South Korean memory chipmaker has rocketed 250% in 2026, fueled by insatiable demand for AI memory chips—and Wall Street analysts say the rally might be only halfway done. With cloud giants racing to expand AI infrastructure and supply constraints keeping competitors at bay, the AI memory cycle appears to have years of runway left.

SK Hynix just delivered one of 2026's most explosive stock performances, and the semiconductor industry's top analysts are raising their price targets rather than calling a top. The memory chipmaker's shares have climbed 250% since January, propelled by what's shaping up to be a multi-year AI infrastructure buildout that shows no signs of slowing.

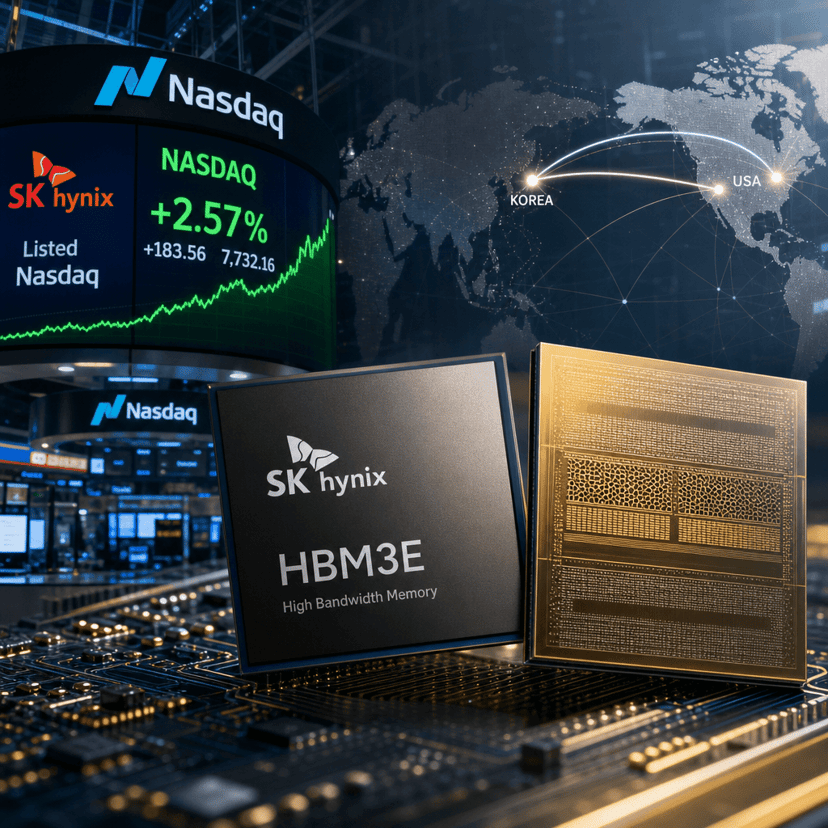

The rally comes as cloud computing giants pour hundreds of billions into AI data centers, creating unprecedented demand for specialized memory chips. SK Hynix's high-bandwidth memory (HBM) has become the critical bottleneck component in Nvidia's H100 and H200 AI accelerators, effectively making the Korean manufacturer an essential player in the AI supply chain.

What's remarkable isn't just the magnitude of the gains—it's the conviction among semiconductor analysts that the move has further to run. Limited manufacturing capacity for advanced memory chips means SK Hynix and rivals like Samsung and Micron Technology can't rapidly scale production to meet demand. That supply-demand imbalance is supporting premium pricing and historic profit margins.

The AI memory cycle operates on a different timeline than traditional semiconductor booms. While previous DRAM and NAND rallies often peaked within 18-24 months, the infrastructure demands of large language models and AI training clusters require sustained capacity expansion over multiple years. Microsoft, Amazon Web Services, and Google Cloud have all signaled aggressive AI infrastructure spending through at least 2028.

SK Hynix's positioning in HBM gives it particular leverage. The company pioneered HBM3E, the latest generation of high-bandwidth memory, and secured early design wins with Nvidia. Manufacturing HBM requires advanced packaging techniques and yields that competitors struggle to replicate quickly. That technical moat translates directly to pricing power—HBM chips command multiples of standard DRAM prices.

The financial impact shows up in SK Hynix's recent quarterly results. Operating margins have expanded dramatically as the company shifts production toward high-value AI memory products. The mix shift away from commodity DRAM and NAND toward specialized AI chips is fundamentally changing the company's profit profile in ways the market is still digesting.

Analysts tracking the semiconductor sector point to capacity constraints as the key driver supporting continued upside. New fabrication plants take 24-36 months to bring online, and clean room expansions require massive capital expenditure. Even with aggressive investment, meaningful new HBM capacity won't hit the market until late 2027 or 2028. That creates a protected window where existing suppliers can capitalize on sustained demand.

The broader AI chip ecosystem reinforces SK Hynix's position. As Nvidia ramps production of next-generation Blackwell GPUs and AMD scales its MI300 accelerators, memory requirements only intensify. Each new generation of AI chips requires more HBM capacity, faster bandwidth, and tighter integration—all areas where SK Hynix has established technical leadership.

Valuation remains a debate among investors. At 250% gains, SK Hynix trades at multiples that would seem stretched in normal semiconductor cycles. But analysts argue this isn't a normal cycle—it's a fundamental infrastructure transition comparable to the cloud computing buildout of the 2010s. If the AI memory super-cycle runs for another three to five years as projected, current multiples could prove reasonable.

The stock's performance is also reshaping South Korea's technology sector. SK Hynix has become the second-most valuable company on the KOSPI index, trailing only Samsung Electronics. The rally has pulled billions in capital into Korean semiconductor stocks and prompted increased attention from global institutional investors.

Risks remain, of course. Any slowdown in AI infrastructure spending would hit memory demand hard. Geopolitical tensions around semiconductor supply chains could disrupt the company's manufacturing or access to key markets. And if competitors bring new HBM capacity online faster than expected, pricing power could erode quickly.

But for now, the setup favors SK Hynix. Cloud providers are locked into multi-year AI infrastructure roadmaps, chip designers need more memory with each generation, and new supply remains years away. That combination has analysts projecting the AI memory rally could have another 100% or more of upside before fundamentals deteriorate.

SK Hynix's 250% rally tells the story of AI's infrastructure demands colliding with semiconductor physics and capital constraints. The memory chips powering today's AI revolution can't be conjured overnight—they require years of investment, technical mastery, and manufacturing scale that only a handful of companies possess. As cloud giants race to build the data centers of the AI era, SK Hynix sits at a critical choke point in the supply chain. Whether the stock doubles again from here depends on how long the AI infrastructure boom sustains and whether new capacity arrives sooner than expected. For now, analysts are betting the cycle has years to run, and the market is pricing in that conviction one record high at a time.