Apple reports fiscal Q1 earnings Thursday, and while analysts expect a blowout iPhone 17 quarter, Wall Street's fixated on a different number: memory costs. The AI-driven component shortage that's sent prices skyrocketing could crush margins just as the company enters what CEO Tim Cook calls a major growth cycle. With the stock down 11% from its December peak despite optimistic revenue guidance, investors want answers on how Apple plans to absorb costs that competitors are already struggling with.

Apple heads into its Thursday earnings call with an unusual problem - too much good news fighting against rising costs. The company already told investors in October it expected revenue to climb 10% to 12% in its fiscal first quarter, which would put the top line somewhere between $136.73 billion and $139.22 billion. That confidence came from strong iPhone 17 early demand during the crucial holiday quarter.

But the stock's down nearly 11% since hitting its December 2 peak, and the disconnect reveals what's really worrying investors. According to Morgan Stanley analyst Erik Woodring, Wall Street hasn't properly accounted for the margin impact of surging memory and storage costs. "We don't believe Street has embedded enough of a margin impact from rising memory costs into its FY26 estimates," Woodring wrote in a Monday note, maintaining his buy rating with a $315 price target.

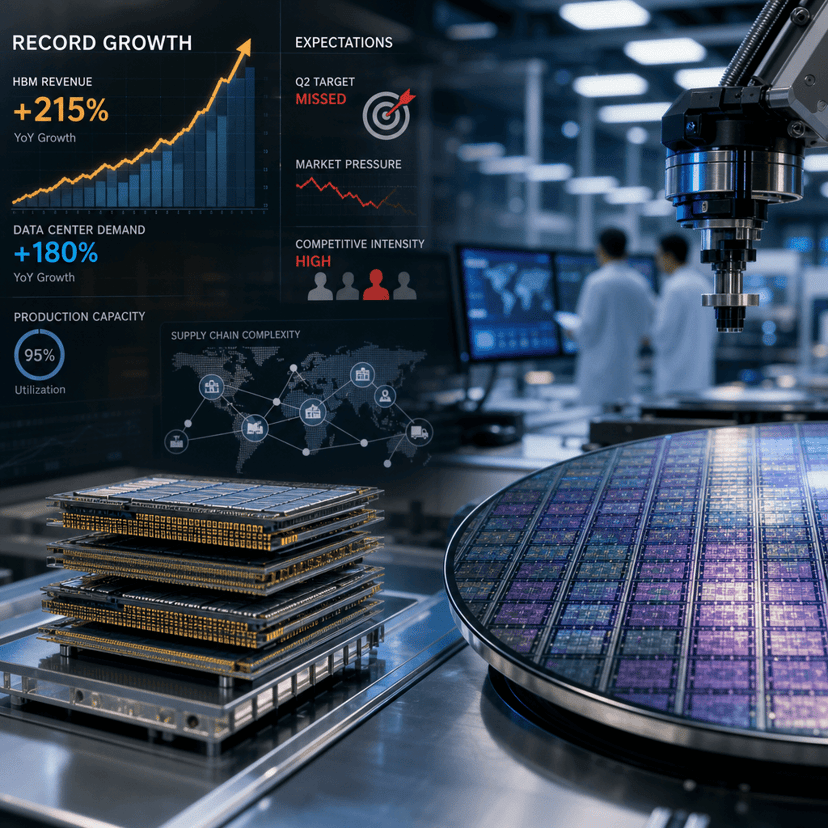

The memory crunch stems from an AI-driven component shortage that's hitting every hardware maker. But Apple faces unique exposure because every product in its lineup - iPhone, Mac, iPad - demands substantial memory and storage. While finance chief Kevan Parekh downplayed the issue in October, saying the company saw "nothing really to note there" on memory pricing, that assessment came before the shortage intensified.

Woodring doesn't expect the cost surge to hit this quarter's results, but warns the impact will mount as the year progresses. "We don't believe consensus still has adjusted to the better than expected iPhone 17 cycle, yet at the same time they haven't adjusted to higher opex and/or gross margin headwinds," he noted. It's a rare moment where Apple might actually beat revenue expectations while disappointing on margins.

The timing couldn't be worse for Apple's AI ambitions. Earlier this month, the company announced it picked Google's Gemini to power parts of its Apple Intelligence software, replacing some internal AI models. The move signaled a pragmatic shift - if Google already built the tech, why duplicate the effort? But it also raised questions about Apple's ability to differentiate its AI offering when it's licensing core functionality from a competitor.

CEO Tim Cook will likely face questions about the highly anticipated Siri relaunch coming later this year. The company's promised a "more personal" assistant that leverages recent AI breakthroughs, but details remain scarce. Investors want to know if this represents genuine innovation or just catching up to Google Assistant and Amazon Alexa capabilities that have existed for years.

Jefferies analyst Edison Lee threw cold water on the entire AI narrative this week, noting that "AI's commercialization and monetization remains challenging" for Apple. He holds a neutral rating on the stock. "Not only is the AI use case not clear for consumers, rapidly rising memory prices would likely make any edge AI applications harder to financially justify in the next two years," Lee wrote Monday. It's a blunt assessment that captures Silicon Valley's broader struggle - AI costs real money to implement, but consumers haven't shown willingness to pay premiums for it yet.

The contradiction plays out in Apple's current position. The company's entering what it calls a major product cycle with the iPhone 17, presumably driven by AI features through Apple Intelligence. But if memory costs keep climbing and consumers don't value the AI capabilities enough to justify higher prices, Apple gets squeezed from both sides. It can't cut features without undermining the growth story, but it can't raise prices without risking volume.

Wall Street consensus expects $2.67 in earnings per share on $138.48 billion in revenue, according to LSEG estimates cited in the CNBC report. The revenue number sits comfortably within Apple's own guidance range, suggesting analysts believe the company will hit its targets. But that EPS figure assumes margins hold steady, which is exactly what multiple analysts now question.

The broader tech sector's watching closely because Apple's component challenges preview what's coming for everyone else. If the most efficient supply chain operator in consumer electronics can't absorb these costs, smaller players have no chance. And if Apple starts signaling margin pressure, it validates concerns that the AI boom's hardware requirements make profitable consumer AI products nearly impossible at current price points.

Thursday's call will reveal whether Parekh still maintains his October stance that memory pricing isn't material, or if the CFO acknowledges the issue's grown more serious. Cook's comments on AI strategy matter too - investors need to hear a coherent plan for how Apple Intelligence drives revenue, not just features. The Gemini partnership suggests Apple might be more willing to license and integrate than build everything itself, which would represent a philosophical shift for a company that's prided itself on vertical integration.

Thursday's earnings call sets up a tension Apple hasn't faced in years - strong product demand colliding with cost pressures it can't easily control. If the company acknowledges margin headwinds from memory pricing, it validates Wall Street's concerns and likely pressures the stock further despite solid revenue growth. If management downplays the issue again, analysts will question whether Apple's being realistic about costs that competitors openly struggle with. Either way, the AI hardware economics problem isn't going away, and Apple's response will signal how the industry's most profitable company plans to navigate a landscape where intelligence costs more than anyone expected.