The memory chip industry just declared an end to decades of painful boom-bust cycles, and the market's buying it. Micron Technology shares have rocketed 370% over the past year, while SanDisk parent Western Digital has surged more than 1,100% - performance that signals something fundamental has changed in the semiconductor business. Industry executives now say artificial intelligence demand has rewritten the rules for memory manufacturers, creating sustained demand that could finally break the industry's notorious cyclical pattern.

Micron Technology just posted the kind of returns that make investors wonder if they've missed something fundamental. The Boise-based memory giant's 370% surge over twelve months looks impressive until you see Western Digital's SanDisk division up more than 1,100% in the same period. But the real story isn't just the numbers - it's what executives are saying about the future.

For decades, memory chip makers rode a brutal rollercoaster. Oversupply crashed prices, companies cut production, shortages drove prices up, everyone ramped capacity, and the cycle repeated. Shareholders got whiplash while manufacturers burned cash trying to time the market. Now industry leaders are claiming AI has fundamentally altered that dynamic, creating demand patterns that look nothing like the PC and smartphone cycles that defined the past 30 years.

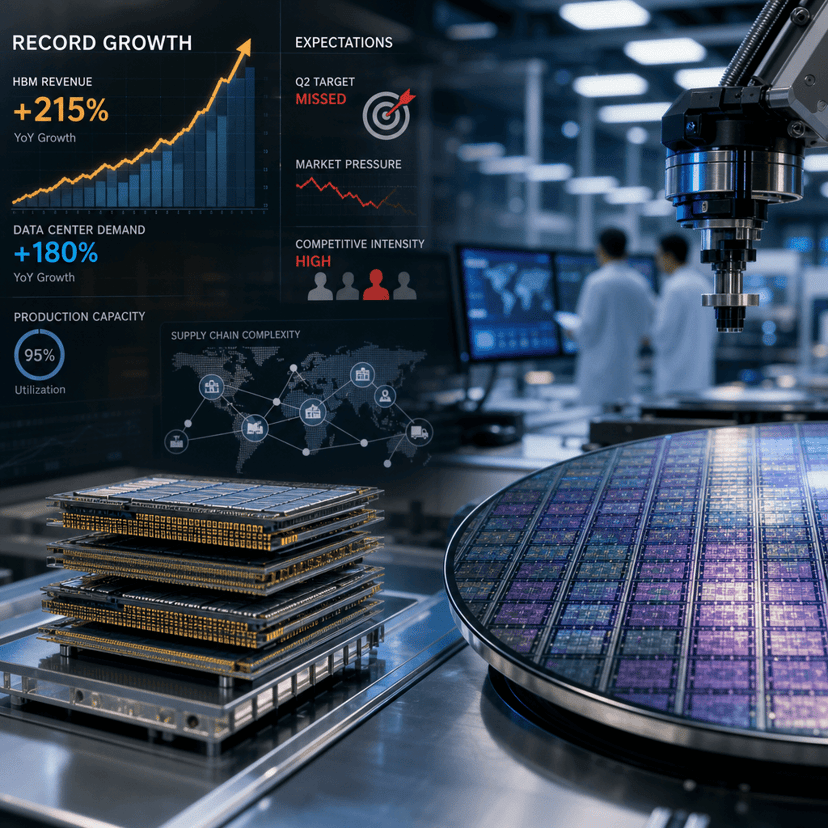

The shift centers on high-bandwidth memory, or HBM - specialized chips that sit right next to AI processors in data centers. Nvidia can't get enough of the stuff for its H100 and H200 GPUs, while AMD and other accelerator makers are scrambling to secure supply for their own AI chips. Unlike consumer memory that sees seasonal fluctuations, HBM demand is growing in lockstep with the AI infrastructure buildout that's consuming hundreds of billions in capital spending.

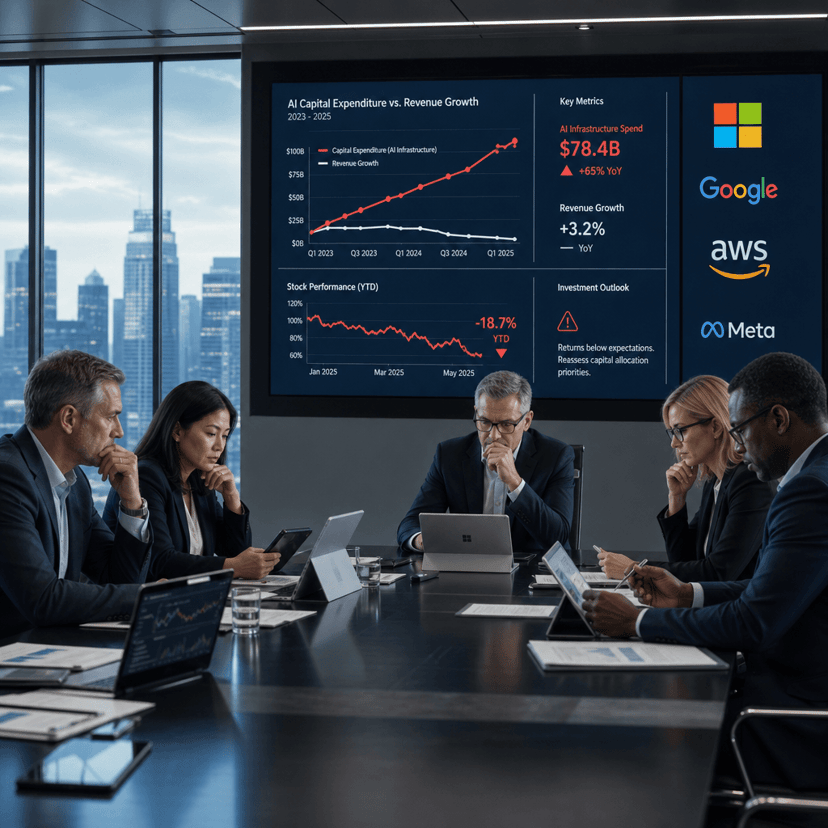

Microsoft, Amazon, Google, and Meta are all racing to expand AI compute capacity, and they're signing multi-year supply agreements that give memory makers unprecedented visibility. That's a dramatic departure from the spot-market pricing that used to dominate the industry, where prices could swing 30% in a quarter based purely on inventory levels.

Micron's stock performance reflects this new reality. The company's been pouring billions into HBM production capacity while maintaining discipline on commodity DRAM and NAND flash - the memory that goes into PCs and phones. That focus on high-margin AI products is exactly what investors want to see, especially after years of watching memory companies destroy value by overbuilding during boom times.

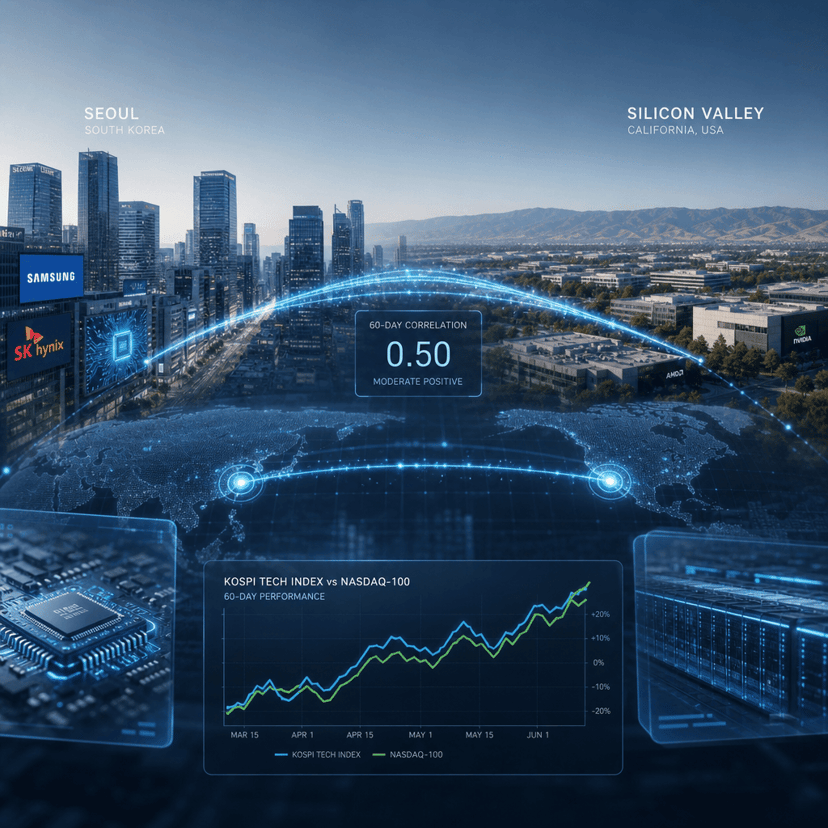

SK Hynix and Samsung, Micron's primary competitors, are making similar bets. The South Korean giants have collectively announced over $50 billion in new memory fab investments focused primarily on advanced packaging and HBM production. The spending spree would normally signal dangerous overcapacity ahead, but this time the hyperscale customers are essentially pre-ordering the output before it even rolls off production lines.

The structural argument makes sense on paper. AI training runs consume memory bandwidth like nothing before, and inference workloads are proving equally hungry as companies deploy models at scale. OpenAI alone is reportedly using thousands of tons of HBM across its training clusters, while enterprise AI adoption is just beginning to ramp. If large language models and AI assistants become as ubiquitous as executives predict, memory demand could grow for years without the traditional cyclical downturn.

But skeptics remember similar promises during previous booms. The cryptocurrency mining craze of 2017-2018 was supposed to create sustained DRAM demand until it evaporated overnight. The 5G smartphone upgrade cycle was meant to drive years of growth before consumers decided their old phones worked fine. Even the pandemic PC boom left manufacturers holding excess inventory when demand normalized faster than expected.

What's different this time is the customer concentration and contract structure. When you're selling to four or five hyperscalers who control the majority of global cloud infrastructure spending, you can negotiate multi-year agreements with volume commitments and price floors. That's fundamentally different from selling into a fragmented PC market where demand depends on consumer spending patterns and inventory levels at dozens of OEMs.

The stock gains also reflect revenge buying after brutal losses. Micron traded below $50 in late 2022 as memory prices crashed and recession fears mounted. Western Digital's transformation from struggling hard drive maker to AI memory player has been even more dramatic, with the SanDisk flash business suddenly looking strategic as AI systems need fast storage to feed training data.

Investors are now pricing in a future where memory companies generate consistent free cash flow and return capital to shareholders instead of burning cash every other year. If the executives are right and AI demand really has broken the cycle, these stocks could still have room to run even after triple-digit gains. If they're wrong and another glut emerges, the selloff will be equally spectacular.

The memory chip industry's claim that AI has ended the boom-bust cycle is compelling, backed by unprecedented hyperscaler demand and multi-year supply contracts that would've been unthinkable five years ago. But the real test comes when the current AI infrastructure buildout matures and companies start optimizing costs instead of racing for capacity. If demand holds and memory makers maintain pricing discipline, this could mark a genuine transformation of one of tech's most volatile sectors. If not, investors who bought at these levels will learn once again why semiconductor stocks demand strong stomachs and long time horizons.