The bond market just flashed a warning sign that equity investors can't ignore. For the first time, fixed-income investors have named an AI bubble as their number one concern, according to a new Bank of America survey released this week. The shift marks a dramatic change in sentiment from institutional money managers who've largely sat on the sidelines of the AI rally, and it signals that worries about frothy valuations are spreading beyond tech-focused equity funds into the traditionally conservative world of bonds.

The bond market has spoken, and it's worried about artificial intelligence. Bank of America's latest investor survey shows fixed-income managers ranking an AI bubble as their primary concern - a first for the monthly pulse check that's been tracking sentiment for years. The finding carries weight because bond investors typically focus on credit risk and interest rates, not equity market froth. When they start worrying about tech valuations, it means they see potential ripple effects across the entire financial system.

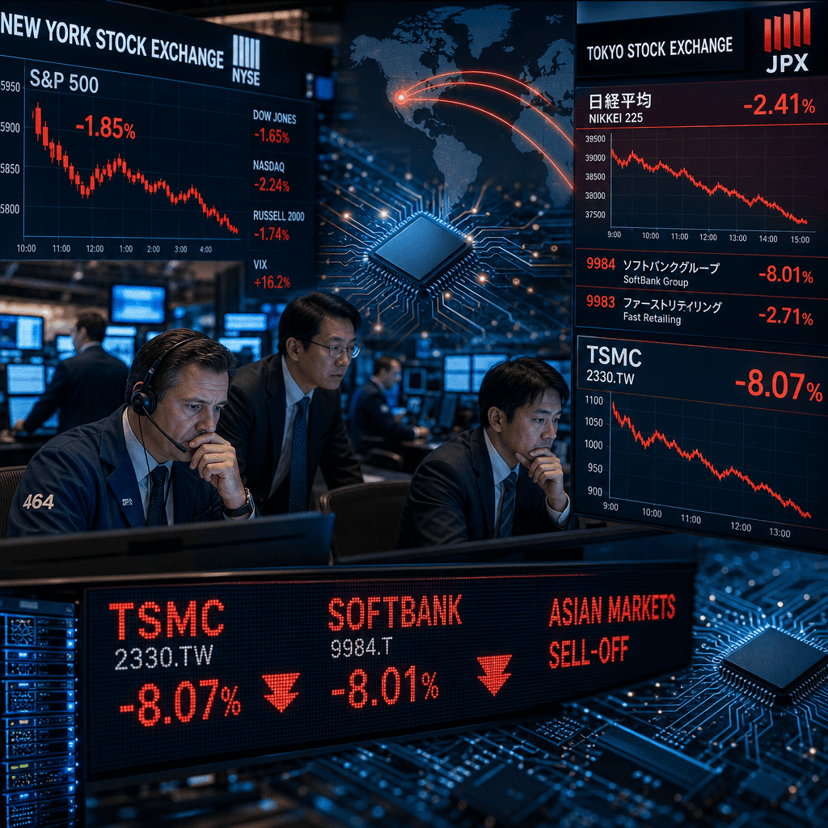

The timing isn't accidental. AI companies have collectively raised hundreds of billions in capital over the past 18 months, with Microsoft, Google, Amazon, and Meta alone committing over $200 billion in infrastructure spending for 2025 and 2026. That money is flowing into data centers, chips from Nvidia, and massive computing clusters - all funded through a mix of cash reserves and corporate debt. Bond investors are now questioning whether the revenue from AI products will ever justify these expenditures.

The concern extends beyond just the tech giants. Smaller AI startups have been issuing debt at aggressive terms, betting that their valuations will continue climbing. But with OpenAI still burning through billions annually despite ChatGPT's popularity, and enterprise adoption of AI tools moving slower than projected, fixed-income managers are starting to price in default risk. According to the Bank of America survey data, bond spreads for AI-focused companies have widened by an average of 45 basis points over the past quarter.

What makes this particularly interesting is the contrast with equity markets, where AI stocks continue to command premium valuations. Nvidia trades at over 60 times earnings, while AI software companies routinely see 15x revenue multiples. Bond investors, who get paid in fixed coupons rather than growth potential, are taking a more skeptical view. They're looking at cash flows, debt loads, and the timeline to profitability - metrics that tell a less rosy story than the narrative driving stock prices.

The survey results suggest professional money managers are reassessing the sustainability of the AI boom. Unlike the dot-com bubble, which was largely confined to public equities, today's AI investment cycle involves massive capital expenditures funded by corporate bonds, bank loans, and private credit. If AI revenues disappoint, the fallout could hit fixed-income holders before equity investors feel the pain. Bond investors remember that during the last major tech correction, highly leveraged companies saw their debt go from investment-grade to junk almost overnight.

But it's not all doom and gloom. The same survey shows that sophisticated investors are looking for opportunities within the AI debt market. Companies with actual revenue traction and reasonable debt levels are being separated from pure hype plays. Infrastructure providers supplying power and cooling to data centers are attracting bond investor interest, as are established tech companies with diversified revenue streams beyond AI. The key distinction is between businesses building sustainable AI operations and those riding a speculative wave.

The shift in sentiment also reflects broader concerns about interest rates and economic stability. With rates higher than they've been in 15 years, companies need to generate real returns to service their debt. AI projects with distant payoff timelines become much less attractive when borrowing costs are elevated. Bond investors are essentially forcing a reality check on the sector, demanding proof that AI investments will generate the cash flows needed to meet debt obligations.

Market veterans are drawing parallels to previous technology cycles, but with important differences. The infrastructure being built for AI - data centers, chip capacity, energy systems - has tangible value beyond any single application. Even if some AI companies fail, the physical assets will remain. That provides a floor for recovery that didn't exist during the dot-com crash. Still, bond investors worry that too much capital is chasing too few proven business models, creating the conditions for a painful shakeout.

The Bank of America survey is already influencing how institutional investors approach portfolio construction. Some are reducing exposure to high-yield tech debt, while others are buying protection through credit default swaps on AI-heavy companies. A few are even finding opportunities to short corporate bonds of firms they believe are overextended. The fixed-income market is essentially placing its bets on which AI investments will survive and which will collapse under their own debt burden.

The bond market's growing anxiety about an AI bubble represents more than just conservative investors being cautious - it's a signal that the financial system is reassessing the sustainability of current AI valuations and spending levels. Fixed-income managers aren't calling for AI to fail, but they're demanding that companies prove they can generate the cash flows needed to justify their debt loads. For the broader market, this shift matters because bond investors often spot cracks in the foundation before equity holders do. Whether this concern proves prescient or premature will depend on how quickly AI revenues catch up to AI spending, but either way, the easy money phase of the AI boom appears to be ending. Investors watching for signs of a broader correction now have a clear indicator: when bond investors start worrying about your sector, it's time to scrutinize the fundamentals.