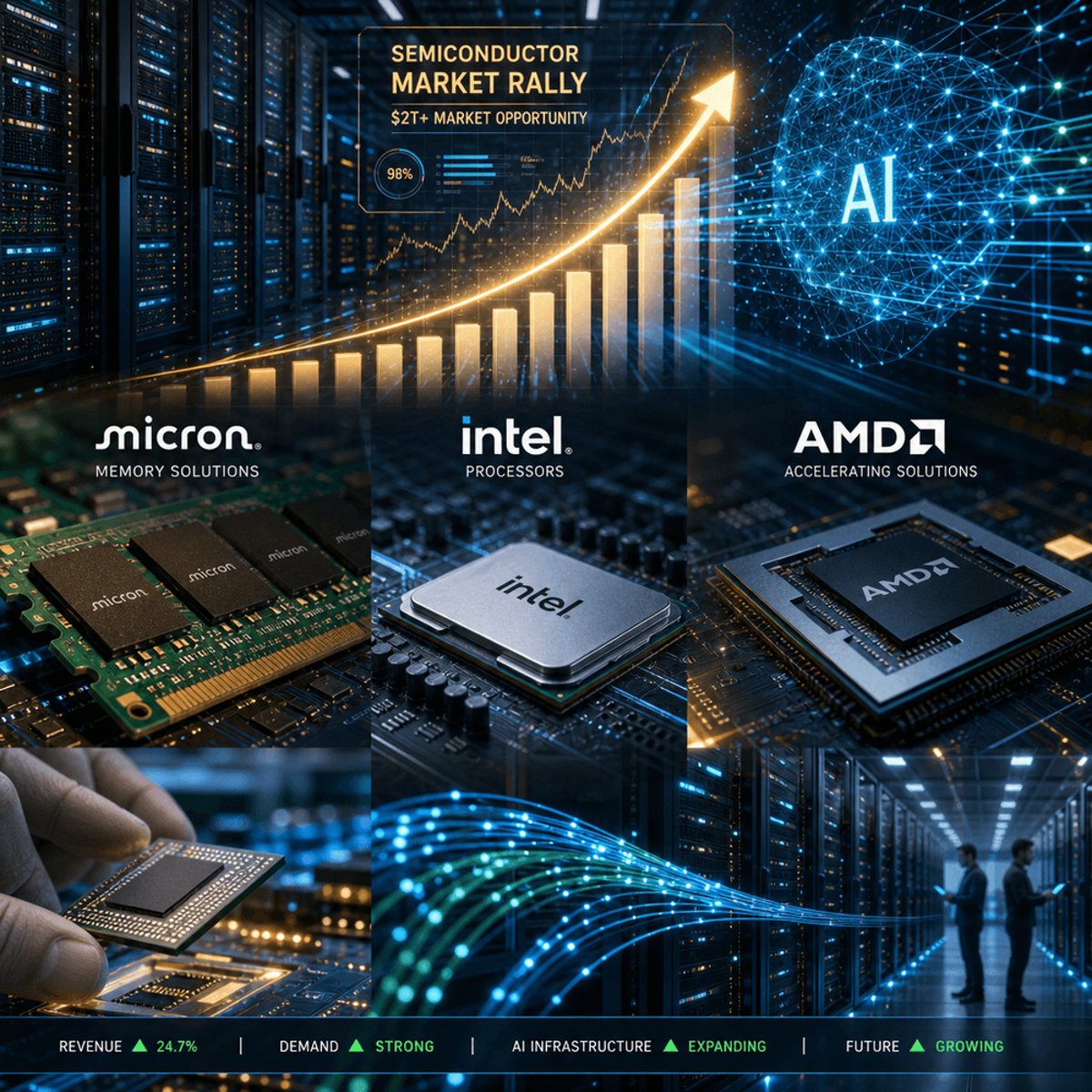

The AI chip gold rush just got crowded. Micron, Intel, and AMD collectively added $2 trillion in market value during Q2 2026, according to CNBC's analysis, as Wall Street finally woke up to the reality that Nvidia won't supply every AI chip on the planet. The surge marks a turning point for the semiconductor sector, where investors are betting big that AI infrastructure needs run deeper than just GPU makers.

Wall Street just rewrote the rules on AI chip investing. While Nvidia dominated headlines for two years, a massive $2 trillion wave of capital flooded into Micron, Intel, and AMD during the second quarter of 2026, according to market data compiled by CNBC. The unprecedented surge reflects a fundamental shift in how investors view the AI infrastructure buildout - it's not just about GPUs anymore.

The rally caught even seasoned semiconductor analysts off guard. Micron, the memory chip giant that spent years in commodity hell, suddenly found itself at the center of AI infrastructure conversations. High-bandwidth memory requirements for AI training and inference drove a revaluation of the entire memory sector. Intel, meanwhile, saw renewed interest in its data center processors and emerging foundry business, while AMD continued capitalizing on its position as the primary alternative to Nvidia's GPU dominance.

This isn't just speculative froth. The AI boom that started with large language models has cascaded through the entire semiconductor supply chain. Every AI data center needs memory chips, networking silicon, power management components, and traditional CPUs alongside the flashy accelerators. Micron's HBM3E memory has become as critical to AI systems as the GPUs themselves, creating supply constraints that pushed the company's valuation skyward.

AMD benefited from two converging trends - enterprises looking for GPU alternatives and the company's strong position in data center CPUs. The firm's MI300 series accelerators gained traction with cloud providers seeking to diversify away from single-vendor dependence. That diversification strategy, once dismissed as wishful thinking, now looks prescient as hyperscalers race to build redundant AI infrastructure.

Intel's inclusion in the rally is perhaps most surprising. The company's AI accelerator roadmap trails competitors, but investors are betting on its Gaudi chips, revitalized foundry ambitions, and the sheer scale of AI-adjacent compute demand. Data centers running AI workloads still need conventional processors for orchestration, data preprocessing, and countless other tasks beyond model training.

The $2 trillion combined gain dwarfs the market cap of many S&P 500 companies. To put that in perspective, the three chipmakers added more value in one quarter than the entire market cap of most Fortune 500 firms. The concentration of wealth creation in semiconductor stocks reflects Wall Street's conviction that AI infrastructure spending will continue accelerating through the decade.

But there's tension beneath the surface. Nvidia still commands premium pricing and massive order backlogs, raising questions about whether competitors can actually capture meaningful revenue share or if investors are pricing in growth that won't materialize. The next test comes with Q2 earnings reports, where revenue and guidance will reveal if the market's enthusiasm matches operational reality.

The rally also signals a maturation of AI investment thesis. Early AI bets focused narrowly on model developers and GPU makers. Now investors recognize the opportunity spans memory manufacturers, networking equipment providers, chip designers, and foundry operators. Micron, Intel, and AMD represent different angles on this broader infrastructure story.

Analysts point to enterprise AI adoption as the next catalyst. While hyperscalers drove initial infrastructure buildouts, thousands of companies are now deploying AI capabilities, creating demand for diverse chip architectures optimized for inference rather than training. That shift favors companies with broader product portfolios beyond pure-play accelerators.

The semiconductor cycle historically punishes investors who chase rallies at peak valuations. Whether this $2 trillion surge marks the beginning of sustained growth or a frothy top depends entirely on whether AI delivers the productivity gains and revenue opportunities that justify current infrastructure spending. For now, Wall Street is betting the boom has room to run.

The $2 trillion Q2 rally across Micron, Intel, and AMD represents more than market exuberance - it's Wall Street acknowledging that AI infrastructure requires an entire ecosystem, not just one dominant GPU maker. The real test comes when earnings reports reveal whether revenue growth justifies these valuations. If hyperscalers and enterprises continue pouring billions into diverse AI hardware, this rally could mark the early innings of a decade-long infrastructure cycle. But if spending concentrates back toward Nvidia or AI adoption disappoints, the recent gains could evaporate as quickly as they appeared. Investors betting on the sector-wide thesis are wagering that AI's appetite for silicon runs deeper than any single company can satisfy.